FBR Digital Invoicing in 2026: Every SRO, Deadline, and Penalty Explained

If your business is registered for sales tax in Pakistan, the FBR digital invoice system is now the law, not a future plan. Every qualifying sale must generate a structured electronic invoice, transmitted to FBR in real time, carrying an FBR invoice number, QR code, and FBR logo. Invoices issued outside the system are treated as invalid, and penalty notices start at Rs 500,000.

Most articles on this topic tell you "it's mandatory, integrate soon." This guide goes further: the complete legal timeline SRO by SRO, the exact phased deadlines, the penalty ladder as enforced, the new 72-hour correction rule, what's coming next under the February 2026 draft rules, and a practical integration checklist.

Disclaimer

This article is for information only and is not legal or tax advice. Always verify the latest notifications on fbr.gov.pk or with your tax advisor, as deadlines and rules change frequently.

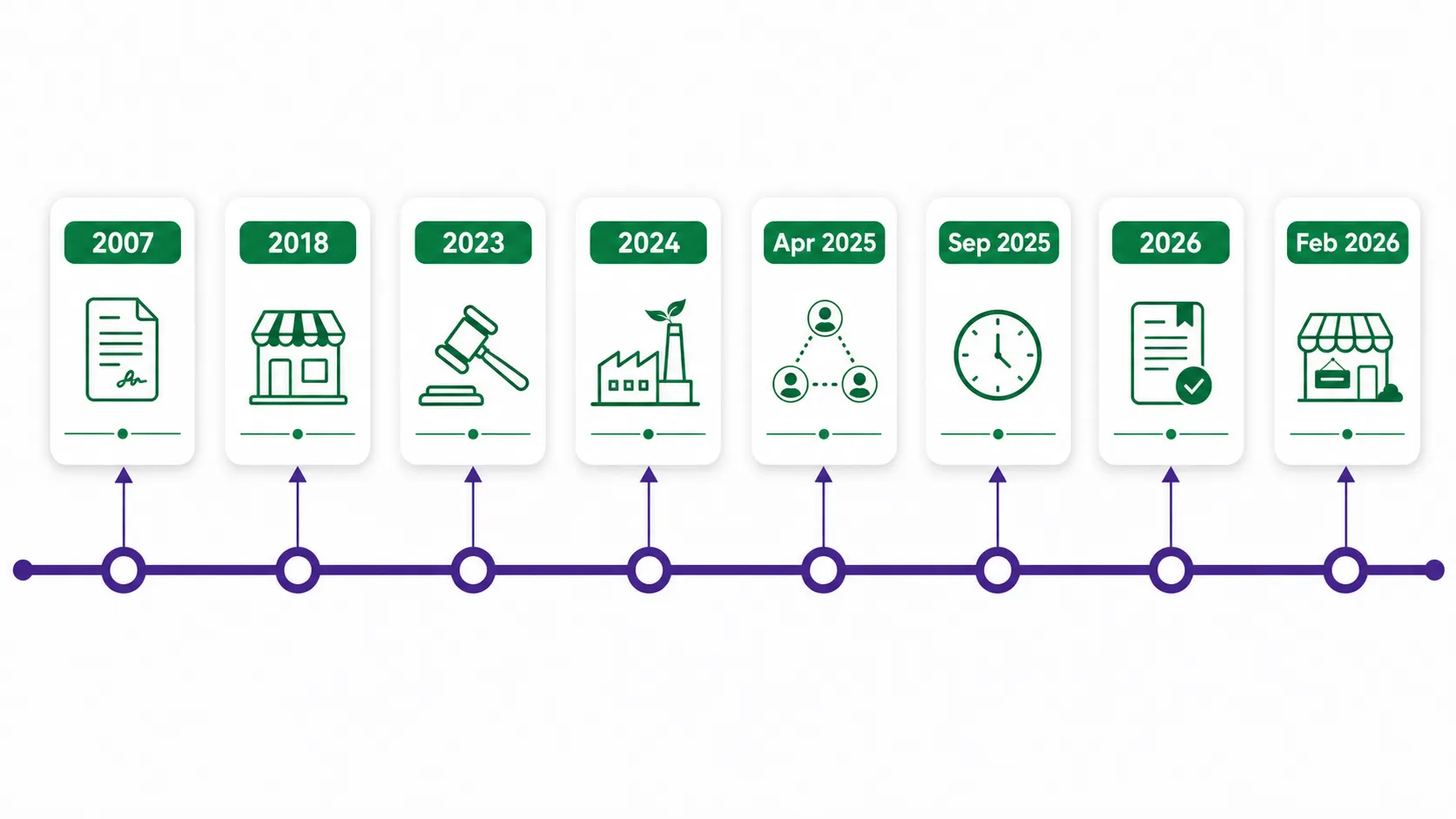

The complete legal timeline: every SRO that built digital invoicing

Understanding where the mandate came from helps you understand where it's going.

| Notification | Date | What it did |

|---|---|---|

| SRO 470(I)/2007 | 9 Jun 2007 | Introduced Chapter XIV of the Sales Tax Rules 2006, the first procedure for electronic invoices |

| SRO 1360(I)/2018 | 12 Nov 2018 | Chapter XIV-AA: mandatory real-time POS integration for Tier-1 retailers (B2C) |

| SRO 1525(I)/2023 | 10 Nov 2023 | Introduced Rule 150Q, the legal foundation of today's e-invoicing regime |

| SRO 28(I)/2024 | 10 Jan 2024 | First rollout, limited to the FMCG sector, effective 1 Feb 2024 |

| SRO 69(I)/2025 | 29 Jan 2025 | Completely replaced Chapter XIV: new rules for integrator licensing, integration, and e-invoice issuance; merged and omitted Chapters XIV-AA and XIV-BB |

| SRO 709(I)/2025 | 22 Apr 2025 | Extended the mandate from FMCG to all corporate and non-corporate sales tax registered persons |

| Extension directive | 30 Apr 2025 | Corporate deadline moved to 1 Jun 2025; non-corporate to 1 Jul 2025 |

| SRO 1413(I)/2025 | Aug 2025 | Superseded SRO 709; introduced turnover-based phases; large taxpayers' go-live set at 1 Sep 2025 |

| SRO 1852(I)/2025 | 24 Sep 2025 | Superseded SRO 1413 with the revised phased schedule (table below), the operative schedule for most businesses |

| STGO 01 of 2026 | 2026 | Confirmed real-time transmission through licensed integrators and restricted invoice corrections to 72 hours of issuance |

| Draft SRO | 18 Feb 2026 | Proposed replacing Chapter VIIA of the Income Tax Rules: pulls specified (service) sectors into e-invoicing/POS integration with QR codes, digital signatures, 24-hour offline-invoice upload, and a formal integrator licensing regime |

The direction is unmistakable: from one sector (FMCG, 2024) to all sales tax registered persons (2025) to service businesses under income tax rules (2026 draft). If you're not covered yet, plan as if you soon will be.

Who must comply, and by when (SRO 1852(I)/2025 schedule)

SRO 1852(I)/2025 set separate dates for registration, sandbox testing, and go-live (issuing e-invoices) by category:

| Category | E-invoicing go-live |

|---|---|

| Public companies, importers, and businesses with turnover above Rs 1 billion | 1 Nov 2025 |

| Non-corporate persons (individuals/AOPs) with turnover above Rs 100 million | 1 Nov 2025 |

| Companies with turnover between Rs 100 million and Rs 1 billion | 15 Nov 2025 |

| Companies with turnover below Rs 100 million | 1 Dec 2025 |

| All remaining registered categories | 31 Dec 2025 |

In other words: every sales tax registered person's deadline has already passed. FBR's enforcement posture through 2026 reflects this: the board expanded audit capacity (hundreds of new auditors recruited by March 2026) and field formations have been issuing penalty notices since 1 September 2025. If you are registered and not yet integrated, you are in the penalty window today.

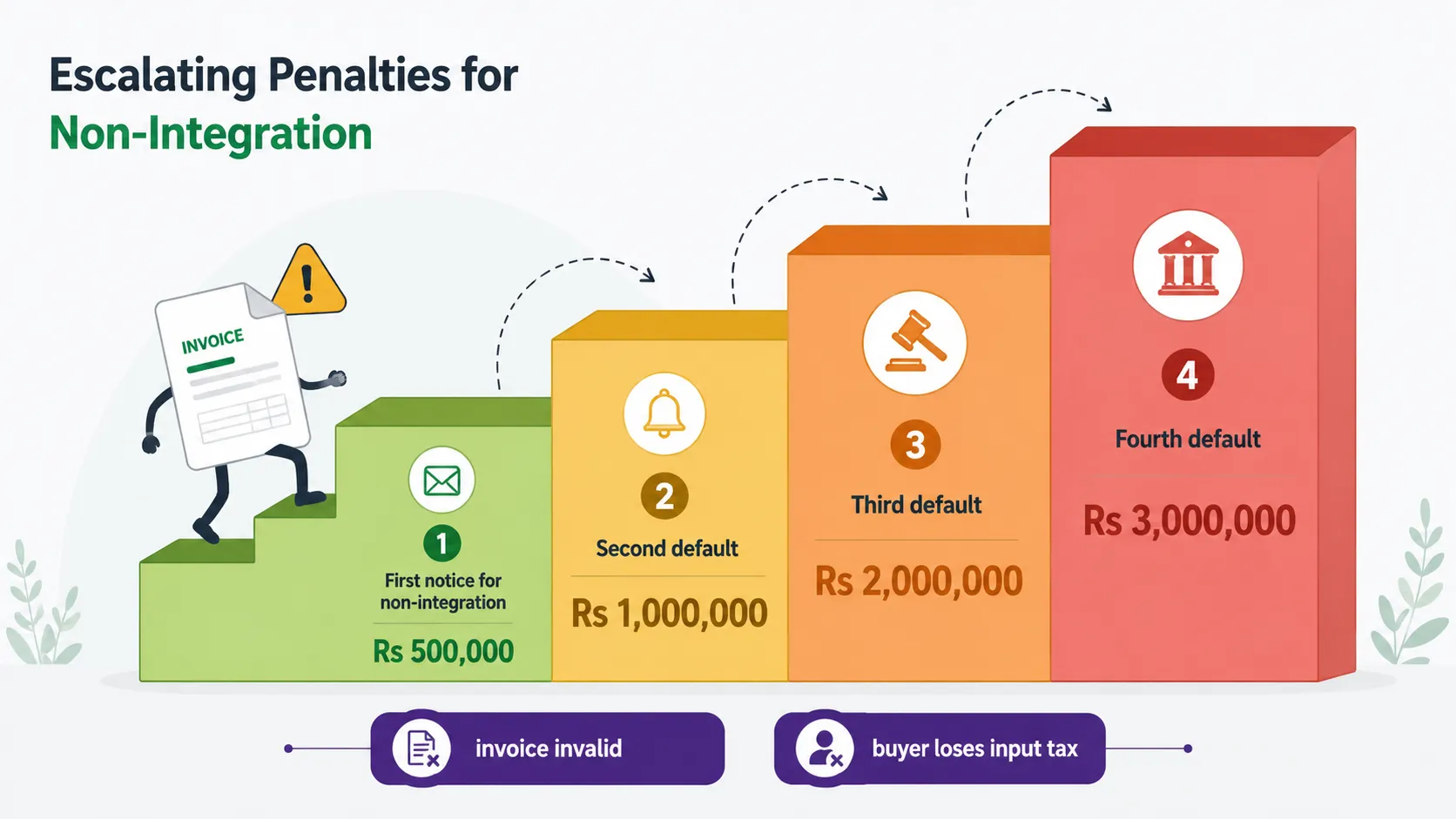

The penalty ladder: what non-compliance actually costs

Penalties apply under Sections 25A and 33 of the Sales Tax Act, 1990, and they escalate per notice:

| Default | Penalty |

|---|---|

| First notice for non-integration | Rs 500,000 |

| Second default | Rs 1,000,000 |

| Third default | Rs 2,000,000 |

| Fourth default | Rs 3,000,000 |

And the monetary fine is only half the damage:

- Your invoices become legally invalid. A sales tax invoice issued outside the digital system by a notified person does not qualify; it's not a compliant tax invoice.

- Your buyers lose input tax adjustment. B2B customers cannot claim input tax against non-digital invoices, so compliant buyers simply stop purchasing from unintegrated suppliers. This commercial pressure usually hits before the penalty notice does.

- Audit exposure rises. Unintegrated registered persons stand out in FBR's data-driven risk system.

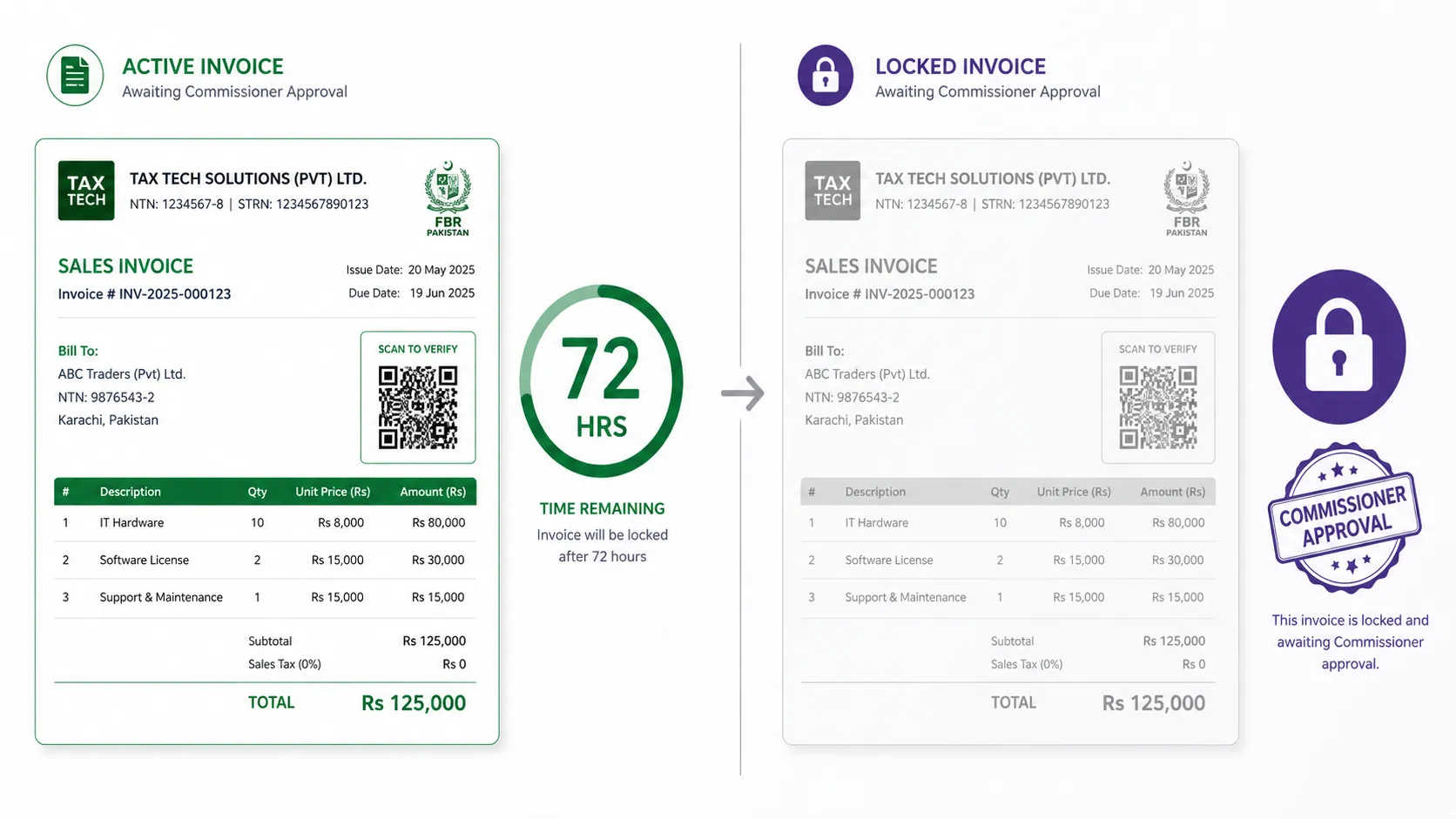

The 72-hour correction rule (STGO 01 of 2026)

A change many businesses missed: once an invoice is issued through the system, corrections are only allowed within 72 hours. After that window, any change requires approval from the Commissioner Inland Revenue. Practically, this means:

- Invoice accuracy at the point of sale now matters far more: item master data (HS codes, tax rates, SKU descriptions) must be clean before you invoice.

- Returns and adjustments must flow through proper credit/debit notes referencing the original FBR invoice number, not retroactive edits.

- Month-end "cleanup" of invoices is effectively dead.

How integration works: your two routes

Route 1: Licensed integrator or integrated software

Under Section 2(15A), a licensed integrator is an entity licensed under Chapter XIV to connect registered persons' systems with FBR. Cloud accounting or invoicing software with built-in integration handles the transmission, FBR invoice number, and QR code automatically. STGO 01/2026 also confirmed a business may use one or multiple licensed integrators. This is the practical route for nearly every SME.

Route 2: PRAL (free)

Under Rule 150XF, PRAL (Pakistan Revenue Automation Ltd) acts as a licensed integrator and provides integration services free of cost. There is no fee payable to FBR itself for integration either; integrator configuration fees are capped by FBR through a sales tax general order. The trade-off with direct PRAL/API integration is technical: your team manages the API connection, sandbox scenarios, and ongoing maintenance.

Step-by-step: integrating your business

- 1Confirm your category and status on IRIS. Your STRN/NTN, business name, and branch details must be accurate; mismatches cause transmission failures. No physical visit to FBR is required; the technical documentation is published on FBR's Digital Invoicing Technical Assistance page.

- 2Choose your route. Pre-integrated software for speed, or PRAL/direct API if you have in-house ERP and developers.

- 3Complete sandbox testing. FBR requires test scenarios to pass before production access: standard-rate invoices, 3rd Schedule goods, exempt and zero-rated supplies, debit notes, and credit notes.

- 4Fix your item master. Every item needs the correct HS code and sale/purchase type. Per FBR's own guidance, items sharing an HS code but with different tax treatment (e.g., standard-rate vs 3rd Schedule goods under HS 2007.9900) must be invoiced as separate line items; clubbing them causes incorrect tax treatment. Different SKUs under one HS code are fine if each has a unique description.

- 5Go live and verify. Issue a live invoice; confirm the FBR invoice number, QR code, and FBR logo print, and that the invoice appears in IRIS. Remember the timing rule: digital invoices must be issued at the time of supply: receipt of payment or delivery of goods, whichever is earlier (Section 2(44)).

- 6Train your team and archive. Handwritten or Excel invoices no longer count; every sale reported in Annexure-C of your return must have a digital invoice. Keep electronic records for six years.

Common integration failures (and fixes)

- Invoice rejected: HS code or rate mismatch. Fix the item master, not the invoice. With the 72-hour rule, upstream data quality is your main defense.

- Buyer NTN validation errors. For B2B invoices, verify the buyer's registration is active before invoicing.

- Connectivity outages. Use software with offline queuing. Under the 2026 draft rules, offline-mode invoices must be clearly marked and uploaded within 24 hours of restoration. Build for that standard now.

- Credit/debit notes not linked. Returns must reference the original FBR invoice number to be accepted.

What's coming next: the February 2026 draft rules

The draft notification issued 18 February 2026 proposes replacing Chapter VIIA of the Income Tax Rules, 2002, extending real-time e-invoicing/POS integration to specified sectors (bringing many service businesses into scope for the first time), with QR codes, digital signatures, record retention, audit access for FBR, outlet/POS registration, and a formal licensing regime for integrators. If your business provides services and you've assumed digital invoicing is "a goods thing," 2026 is the year that assumption expires.

How TaxHub keeps you compliant

TaxHub was built for exactly this regime. With TaxHub's FBR digital invoicing, every invoice transmits to FBR in real time via PRAL/IRIS with the FBR invoice number and QR code generated automatically; all 28 FBR invoice scenarios (SN001 to SN028), sandbox testing, HS-code-aware item masters, linked credit/debit notes, and Annexure J & H registers are handled inside a full accounting and tax compliance suite, so your Annexure-C and sales tax return reconcile from the same data.

Already past your deadline?

Setup takes hours, not weeks. See pricing or book a demo.

FAQs

What is SRO 709(I)/2025?

The 22 April 2025 notification (under Rule 150Q) that extended mandatory e-invoicing from the FMCG sector to all corporate and non-corporate sales tax registered persons. Its schedule was later superseded by SRO 1413(I)/2025 and then SRO 1852(I)/2025.

What is the penalty for not integrating with the FBR digital invoice system?

Notices start at Rs 500,000 for the first default and escalate to Rs 1,000,000, Rs 2,000,000, and Rs 3,000,000 for subsequent defaults under the Sales Tax Act, 1990. Non-digital invoices are also invalid, costing your buyers their input tax adjustment.

Is there any government fee for integration?

No fee is payable to FBR. PRAL provides free-of-cost integration under Rule 150XF, and licensed integrators' configuration fees are capped by FBR.

Can I correct an invoice after issuing it?

Only within 72 hours under STGO 01 of 2026. Beyond that, changes need Commissioner Inland Revenue approval; use credit/debit notes instead.

Does digital invoicing apply to services?

The sales tax mandate primarily covers goods (Islamabad territory covers services too), but the February 2026 draft rules under the Income Tax Rules propose bringing specified service sectors into real-time e-invoicing.

Does digital invoicing replace my sales tax return?

No, you still file monthly, but every sale in Annexure-C must correspond to a digital invoice, which makes reconciliation faster and mismatches visible immediately. See the 2026 return deadlines so nothing catches you off guard.

Try TaxHub free: get FBR compliant in 10 minutes

Real-time FBR digital invoicing, complete accounting, and a dashboard that's entirely yours. No credit card required.

Request Free Demo